UEFA Club Competition reforms over the years: Analysing the impact on clubs in small and medium-sized markets

Article written by Football Benchmark

UEFA Club Competitions (UCC) are widely regarded as the pinnacle of club football. For most clubs, however, participation on this stage is anything but guaranteed and often celebrated as a landmark achievement. Automatic access to the UEFA Champions League (UCL) league phase is restricted to the top ten leagues by UEFA’s country coefficient. However, the remaining 45 nations, home to nearly 200 million people, are a fundamental component of European club football, providing diversity, depth, and identity to the continental game.

As the revenue and performance gap between Europe’s largest markets and the rest continues to widen, UCCs have evolved in an effort to balance the growth demands of elite clubs with the need to preserve access and diversity across the continent.

This article analyses how clubs from small and medium-sized markets have fared over the past two decades, looking at participation and performance while assessing the impact of competition reforms between 2005/06 and 2024/25 on these clubs.

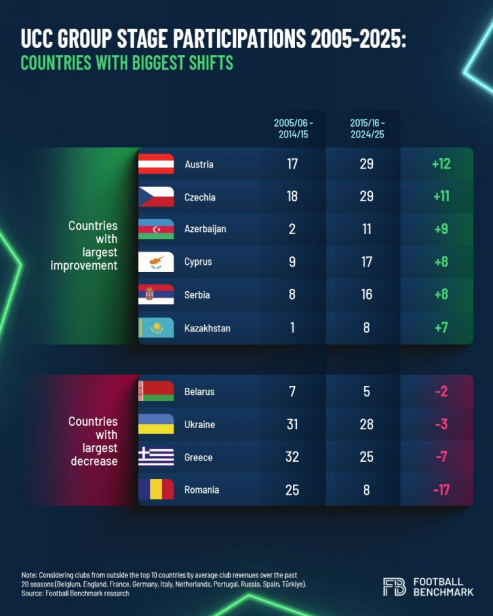

For the purposes of this analysis, “small and medium-sized markets” are defined as the 45 UEFA nations outside the top ten by average club revenues over the past 20 seasons (Belgium, England, France, Germany, Italy, Netherlands, Portugal, Russia, Spain and Türkiye).

Overview of UCC reforms

Understanding the impact of reforms requires a look at the major changes to UCCs over the past two decades.

In 2009/10, UEFA rebranded the UEFA Cup as the Europa League (UEL), expanding the group stage to 48 teams, taking the overall number of participating clubs across both competitions from 72 to 80. This restructuring also introduced the “Champions Path” to the UCL, which gave domestic champions from smaller leagues a better chance of reaching the group stage by separating them from stronger non champion clubs of top leagues. This structure effectively defined the competition model for more than a decade.

In 2021/22, the UEFA Conference League (UECL) was launched as a third-tier competition to widen access for more countries, increasing overall participating clubs to 96, while reducing the UEL to 32 teams and making qualification more competitive. In 2024/25, the competitions expanded to 108 clubs with the introduction of the “Swiss system”, replacing traditional group stages with a league phase and adding more matches to the calendar. 28 new places were added between 2020/21 and 2024/25, a 35% increase representing the most significant expansion in the history of European club competitions.

Group stage performance trends

An analysis of UCC group stage and league phase appearances shows that competition reforms have been a major driver of participation for the markets under review, with most newly created slots being filled by these 45 nations. Before the 2009/10 UEL expansion, they averaged 24 clubs per season, representing 33% of the total. This rose to 30 (38%) after the reform. The introduction of the UECL brought a similar uplift, with an average of 43 clubs (45%) during 2021 to 2024. Their share increased again with the expansion last season when a record 53 clubs (49%) came from these markets.

As a result, all but five of the 45 small and medium-sized markets have had at least one representative in the group stages of UCCs over the past 20 seasons. The only exceptions are Andorra, Georgia, Malta, Montenegro and San Marino. This reflects the growing inclusiveness of the competitions.

Despite this growing presence overall, representation in the UCL and UEL has largely stagnated over the past two decades, with little growth even after the 2024/25 expansion. The increase in access and participation has therefore been concentrated almost entirely at UECL level.

At the same time, the evolution of participation across these markets has not been uniform. Some countries have capitalised on newly created opportunities earned on the pitch, while others have seen their presence decline.

Austria and Czechia stand out as the biggest climbers, not only increasing their number of participants but also seeing clubs such as RB Salzburg and SK Slavia Praha reach the knockout stages of the UCL and UEL on occasions. In Azerbaijan and Serbia, progress has been primarily driven by a small number of dominant clubs, with Qarabağ FK, FK Partizan Beograd, and FK Crvena Zvezda accounting for most appearances. Cyprus has been the notable exception, with seven different clubs featuring over the past decade.

At the other end of the spectrum, Romania’s decline has been particularly stark. After having a team in the UCL group stage every year between 2006/07 and 2012/13, the country’s teams have not returned since. Greece has also lost ground, although it still averaged 2.5 clubs per season in UCCs in the past decade.

Round of 16 qualification trends

Looking beyond participation, qualification for the knockout stages highlights how competition design has also shaped the performance and competitiveness of clubs from these markets.

In the UCL, breakthroughs have become increasingly rare: since 2018/19, only RB Salzburg (2021/22) and FC Copenhagen (2023/24) have reached the Round of 16. The UEL, once a more level playing field during its 48-team group stage era, has also seen a declining trend. Over the past four seasons, 13 teams reached this stage, with eight advancing to the quarter-finals, four to the semi-finals, and only Rangers FC making a final.

By contrast, the UECL has quickly established itself as a genuine platform for new stories of success. At least six clubs from these markets have reached the Round of 16 in each edition, with a record ten in 2024/25. Three have advanced to the semi-finals (FC Basel in 2022/23, Olympiacos CFP in 2023/24, and Djurgårdens IF Fotboll in 2024/25), and Olympiacos even lifted the trophy in 2023/24, the first and only continental title for a club from these markets since 2009.

Despite recent on-pitch success, the combined number of teams advancing beyond the group stage in the UCL or UEL has not exceeded eight in any season, and only five since 2021/22, suggesting redistribution rather than an overall increase in competitiveness. On the other hand, the recent removal of traditional “drop-down” routes between competitions in the most recent reforms could, however, further expand opportunities for clubs from smaller and medium-sized markets in the years ahead.

Expanded access and the challenge of imbalance

All things considered, it is evident that UCC reforms have expanded access for small and medium-sized markets, creating growth opportunities that domestic leagues alone often struggle to provide. This additional platform offers clear benefits: increased visibility for sponsors and broadcasters, enhanced credibility in the transfer market, and stronger appeal to both domestic and international talent seeking European exposure. For many clubs, consistent participation also accelerates professionalisation, attracts investment, and raises organisational standards.

Under the new model, leading clubs in these regions enjoy more regular participation, enabling longer-term financial planning and revitalising local fan engagement. At the same time, recurring UCC income is reinforcing the emergence of entrenched national ‘super clubs’ in certain markets. Clubs such as Ferencvárosi TC in Hungary, PFC Ludogorets Razgrad in Bulgaria, and Qarabağ FK in Azerbaijan already exemplify this dynamic.

Yet this new continental “middle class” of clubs faces a structural challenge: while they increasingly dominate their domestic leagues, widening the gap with local peers, they continue to struggle against teams from Europe’s top markets whose resources remain far greater.

With the new format now in its second year, the upcoming season will provide valuable insights into how outcomes align with original objectives. In the near term, clubs will continue to benefit from greater exposure and growth linked to UCC participation. Over time, however, the consolidation of their position may reignite debate around the need for stronger regional competitions. For stakeholders, the key challenge remains ensuring that the benefits of expanded participation translate into broader and more sustainable growth across national and regional ecosystems beyond the elite markets.

By Football Benchmark